Annex 1: Economic and Fiscal Outlook

Introduction

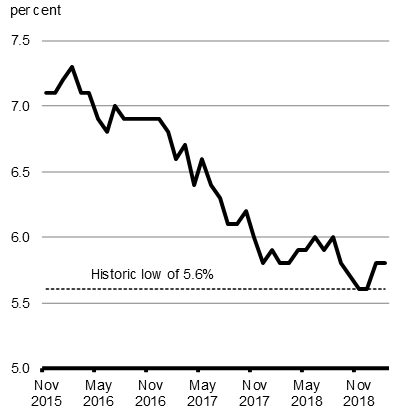

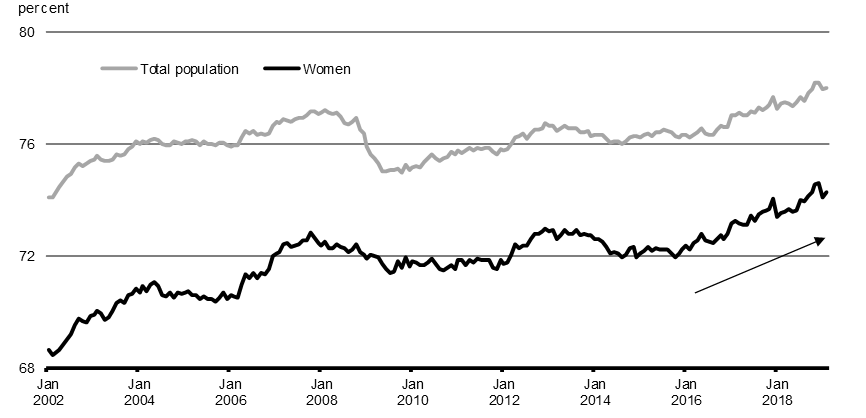

In a challenging global economic environment, Canada’s economy remains sound. Targeted investments in the middle class and strong economic fundamentals have contributed to strong job creation and resulted in an unemployment rate that has reached its lowest levels in more than four decades (Chart A1.1).

Since November 2015, the hard work of Canadians has helped to create over 900,000 jobs. In 2018, there were more Canadians employed, as a share of the working-age population, than at any moment in Canada’s history. Underlying this strong performance have been strong employment gains by women, with the pace of job gains for women more than doubling since November 2015, compared to the previous three-year period.

In recent months, the outlook for global growth has become more uncertain and financial market volatility has risen. From a global perspective, economic activity is estimated to have peaked earlier in 2018, with momentum slowing somewhat more than expected since that time. At home, a more uncertain global economic environment, lower oil prices and higher interest rates have also contributed to softer economic growth at the end of 2018.

Despite these challenges, Canada began 2019 with the strongest two-month stretch of job creation since 2012. The economy is expected to strengthen over the second half of 2019, and to remain among the leaders for economic growth in the Group of Seven (G7) in both 2019 and 2020.

Canada’s trade advantage is also expected to pay dividends in the coming years. With the successful conclusion of the new NAFTA—the Canada-United States-Mexico Agreement—as well as the Canada-European Union Comprehensive Economic and Trade Agreement (CETA) and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), Canada is now the only G7 country to have free trade agreements with all other G7 nations, and now has comprehensive free trade agreements with countries representing nearly two-thirds of the world’s total gross domestic product (GDP).

This trade strength, combined with new tax incentives to encourage businesses to accelerate investment in capital goods, will support a strengthening in business investment in Canada going forward.

At the same time, it is clear that there is more work to be done to ensure that the middle class and people working hard to join it are able to share in Canada’s economic success. The Government’s commitment to investing in the middle class continues.

Recent Economic Developments

Global economic expansion is moderating

For the past two years, global economic activity has been strong and broad-based across most regions of the world. This has helped push the unemployment rate among Organisation for Economic Co-operation and Development (OECD) countries to its lowest level since 1980.

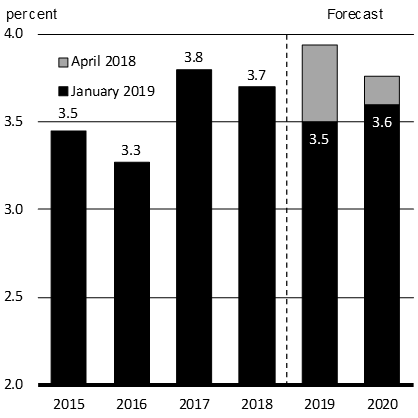

The International Monetary Fund (IMF) estimates that the global economy grew by 3.7 per cent in 2018, largely reflecting growth seen in emerging economies (Chart A1.2). However, it is likely that global growth peaked in 2018, as business activity has slowed in virtually all major advanced economies.

A shift to a slower pace of global economic activity was expected. However, growth slowed more than anticipated in Europe in the second half of 2018, with Germany’s economy registering virtually no growth and Italy entering a technical recession (i.e., two consecutive quarters of contraction in real GDP).

In the United Kingdom, where uncertainty over the country’s planned exit from the European Union has prevailed, economic growth slowed markedly at the end of 2018. Meanwhile, a number of recent indicators for China and other emerging economies have underperformed, potentially signalling weaker-than-expected economic momentum in these regions as well.

Taken together, many of these developments contributed to the IMF marking down its latest outlook for global growth. It now projects that global growth will slow to about 3.5 per cent in both 2019 and 2020, down from average annual growth of 3.8 per cent in the past two years.

In the U.S., the pace of economic growth is expected to moderate to 2.4 per cent in 2019 (compared to 2.9 per cent in 2018), and to 1.7 per cent in 2020, in part reflecting waning fiscal stimulus. However, a number of the factors that underpinned U.S. growth in 2018 are expected to carry forward into 2019, including job and wage gains, which will continue to support consumption growth.

Global growth concerns contributed to increased market volatility at the end of 2018

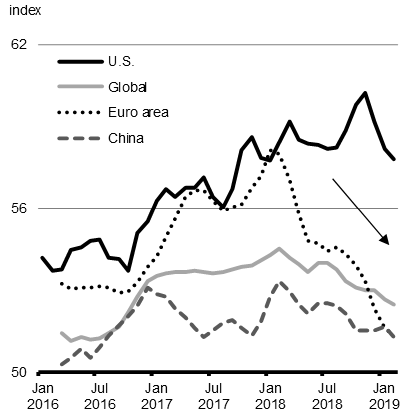

Slowing global economic growth, combined with policy uncertainty related to the U.S. government shutdown and ongoing tensions between China and the U.S., led to a drop in business and consumer confidence at the end of 2018. These factors, along with lower expectations for corporate earnings, translated into increased financial market volatility. The result was sharply lower global equity valuations, declining government bond yields and a moderate rise in corporate credit spreads, as markets began to reprice these developments.

In addition, over the past year, the evolution of some financial indicators has raised concerns about the prospects for future growth. In particular, the flattening of the U.S. yield curve, which has been associated with impending recessions in the past, has exacerbated concerns over the current expansion.

Since the end of 2018, the performance of global equities has improved and other financial conditions have eased. This includes a rise in U.S. equities after the Federal Reserve signalled a more patient approach to further monetary policy normalization amid slowing external demand and market volatility.

Canada’s economy remains strong, focus on middle class growth remains essential

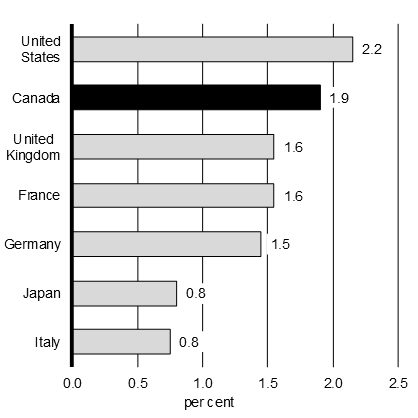

Canada faces the current environment of global uncertainty and softer economic growth at the end of 2018 from a position of strength. Canada led the G7 in growth in 2017 and was second only to the U.S. in 2018. Going forward, the IMF expects growth in Canada to remain among the leaders in the G7 in both 2019 and 2020.

Labour market conditions are at their strongest in decades. Throughout 2018, another year of solid employment gains left the unemployment rate at its lowest levels in over 40 years. Since November 2015, the hard work of Canadians has created over 900,000 jobs. About three-quarters of these new jobs have been full-time positions; in 2018 alone, all employment gains were full-time positions.

Underlying Canada’s strong employment growth have been strong gains by women, with the pace of job gains for women more than doubling since November 2015, compared to the previous three-year period. This contributed to lifting the share of working-age Canadians who are employed to a record high in 2018 (Chart A1.3). It is also helping to offset the pressures of an aging population, which is weighing on the overall employment-to-population ratio.

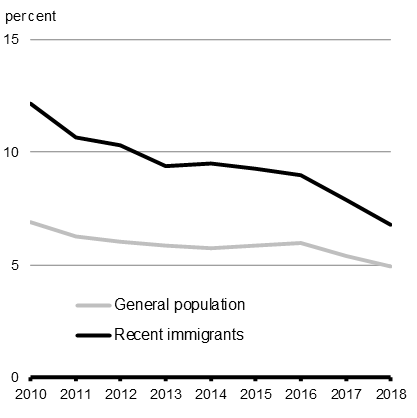

Recent improvements in employment have also been shared among groups of Canadians who are often underrepresented in the labour market. These include recent immigrants, single mothers, Indigenous Peoples living off-reserve, youth and individuals with lower educational attainment. Today, the share of working-age Canadians who are employed is close to or higher than its pre-recession level for most of these underrepresented groups.

Continued employment gains lifted the share of working-age Canadians who are employed to a record high in 2018

Amid strong labour market conditions, a relatively high number of employers in the Bank of Canada’s latest Business Outlook Survey continued to report labour shortages, indicating that they continue to struggle to find the people they need to grow their businessesand meet rising demand. These tight conditions contributed to an upturn in wage growth in 2017, and supported another solid gain in 2018—among the fastest paces of growth witnessed in the past eight years.

In oil-producing provinces—Alberta, Saskatchewan and Newfoundland and Labrador—wage growth notably softened over the second half of 2018, pulling down the national average. Overall, employment and wage growth in these provinces continues to be affected by the lasting effects of lower world oil prices.

Encouragingly, employment in both Alberta and Saskatchewan increased in 2018 across a number of industries, including the sub-sector linked to oil and gas extraction. However, unemployment rates in these provinces remain well above levels seen before the significant decline in oil prices that began in mid-2014.

Focus: Canada’s newcomers are ready to work and help grow the economy

In 2018, Canada’s population grew by 1.4 per cent—the strongest showing in almost three decades. The welcoming of a growing number of immigrants has played an important role in driving Canada’s strong population growth.

Historically, Canada has relied on newcomers as a key source of population and economic growth. On a net basis, international migration accounted for about 70 per cent of Canada’s population growth over the past two decades and close to 80 per cent of total population growth in 2018.

As the Canadian population ages, projections show that the contribution of immigration to Canada’s population growth will increase rapidly in the next few years. Without immigration, Canada’s population would start to decline in slightly more than a decade, and real GDP growth would slow to about 1 per cent per year. Attracting talented workers from around the world will be essential to help grow our economy and improve the living standards for all Canadians.

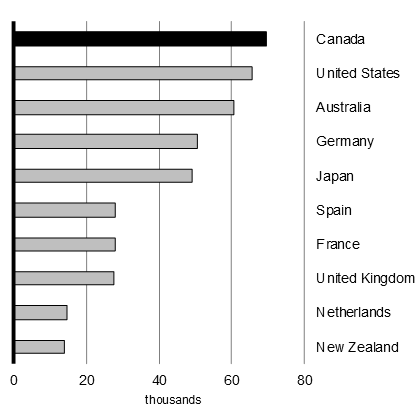

The economic benefits of immigration depend on how well newcomers integrate into the labour market. Canada is doing well in this regard with the highest entry of immigrants ready and able to work among OECD countries (Chart A1.4). Furthermore, newcomers to Canada have steadily improved their integration into the labour market over the past three years. Canada’s approach to gradually increasing immigration levels—both to support Canada’s labour market needs and to provide assistance to refugees and support family reunification—has helped new Canadians smoothly integrate into the labour market and supported businesses and communities across the country.

(Population Aged 25-54)

Household spending has cooled, and housing markets are more balanced

The Canadian economy grew roughly 2 per cent in 2018, in line with the economy’s long-term, potential pace of growth and consistent with an economy and labour market operating close to capacity.

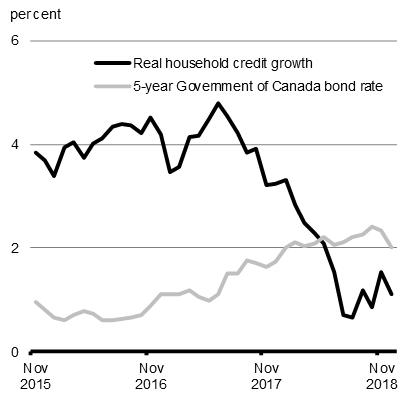

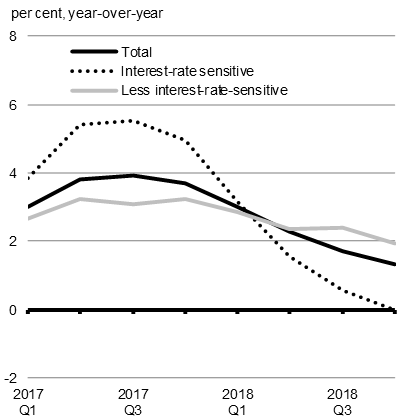

Across the country, households are adjusting to overheating in some regional housing markets, higher interest rates and mortgage regulation changes. In turn, household credit growth has eased to more sustainable levels (Chart A1.5).

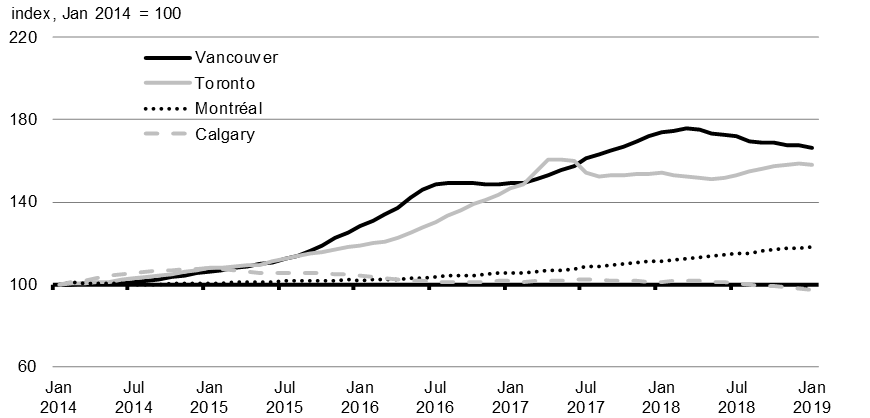

Following the overheating that occurred in 2016 and 2017 in the Toronto and Vancouver housing markets, sales have moderated and price growth has softened (Chart A1.6).

Housing markets are undergoing an orderly correction, though affordability challenges remain in Toronto and Vancouver

The fundamentals remain supportive of business investment

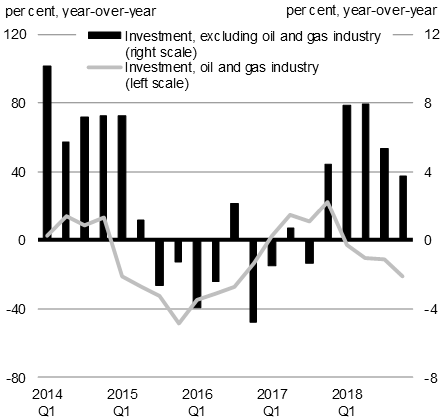

Building on improved momentum since the end of 2016, business investment grew for a second consecutive year in 2018, reflecting growth outside of the oil and gas industry (Chart A1.7).

In recent quarters, business investment has moderated amid slowing global economic activity and trade, and heightened uncertainty over the global growth outlook. Business investment in Canada is expected to improve going forward, supported by continued gains in domestic and foreign demand. The signing of new and modernized trade agreements, including the new NAFTA—the Canada-United States-Mexico Agreement—and new tax incentives proposed in the 2018 Fall Economic Statement to encourage businesses to accelerate investment in capital goods, including the Accelerated Investment Incentive, also support this outlook.

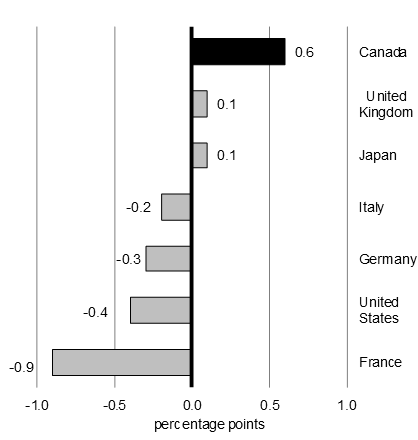

At the same time, Canada’s attractiveness as a place to do business is evidenced by year-to-date flows of foreign direct investment (FDI) to Canada in 2018. For this period, Canada was the only G7 country to witness a material improvement in foreign direct investment into the country. For the same period, foreign direct investment inflows worldwide declined by roughly 25 per cent.

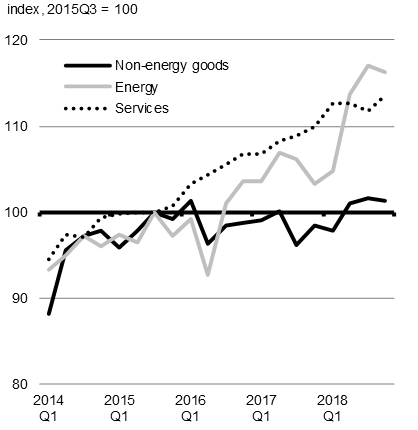

Export growth continues to be led by energy and services

In recent years, modest increases in total real exports have been driven in large part by exports of energy commodities and services (Chart A1.8). Meanwhile, despite a recent uptick, non-energy exports have grown little over the last two years.

Going forward, exports will continue to be supported by rising foreign demand and a weak Canadian dollar. However, ongoing trade policy uncertainties will continue to act as headwinds to Canada’s export performance.

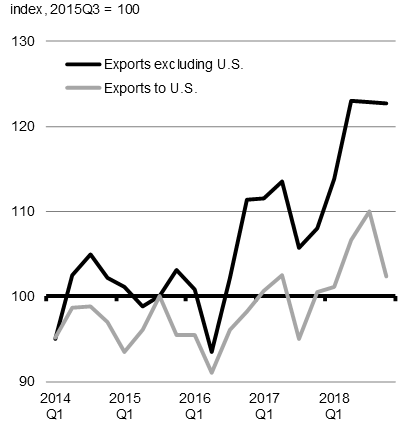

Encouragingly, recent data suggests that growth in exports to non-U.S. markets—particularly for those directed to European countries—has outpaced growth in exports to the U.S. This development is supported by the coming into force of the Canada-European Union Comprehensive Economic and Trade Agreement. Further diversification will be supported by the Comprehensive and Progressive Agreement for Trans-Pacific Partnership, which entered into force on December 30, 2018.

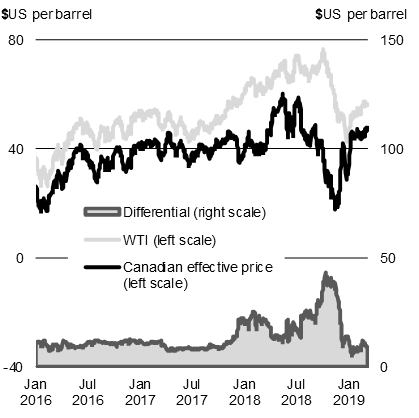

Lower global oil prices are dampening growth

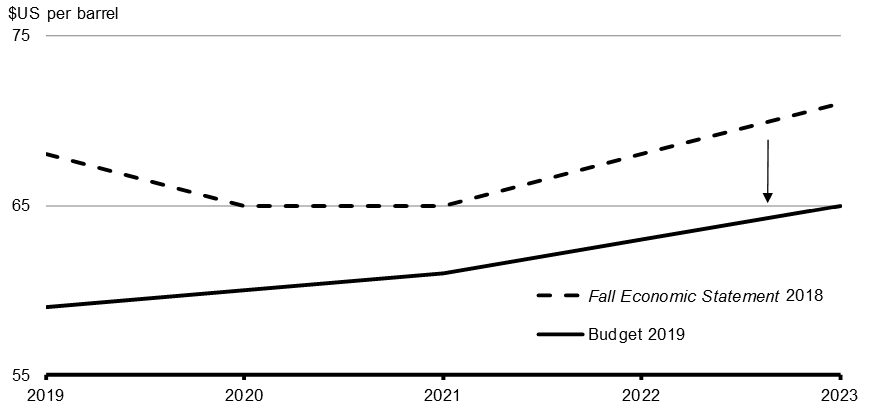

In early October, major world oil benchmark prices began to drop after hitting their highest levels in nearly four years. The decline has largely been attributed to surging oil output in the U.S., along with weaker-than-expected enforcement of U.S. sanctions against Iran and expectations of slower global growth. The price of West Texas Intermediate (WTI) crude oil has recently improved to about US$55 per barrel—but remains roughly 25 per cent below its early-October peak, and well below expectations in the 2018 Fall Economic Statement (Chart A1.9).

The outlook for world oil prices remains very uncertain. On the one hand, crude oil supply, particularly out of the U.S., could continue to exceed expectations. This would exert further downward pressure on world prices. On the other hand, there remains uncertainty around supply and export patterns from Organization of Petroleum Exporting Countries members and their allies, as well as around the balance of world oil markets in a context of ongoing tensions involving both major importers and exporters of crude oil.

Crude oil prices have fallen below expectations outlined in the 2018 Fall Economic Statement and remain vulnerable to world market developments

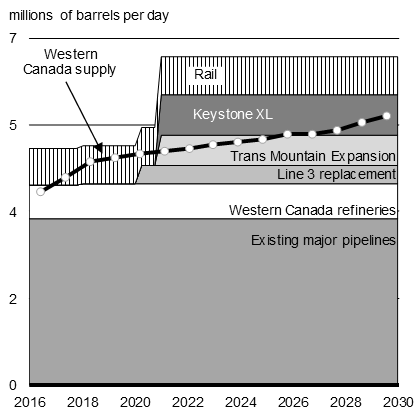

Canadian energy producers face additional volatility in Canadian oil prices, reflecting ongoing production growth amid constrained transportation capacity. Since 2017, the growing supply of crude oil from Western Canada has exceeded available export pipeline infrastructure and the region’s refining capacity (Chart A1.10). As a result, record levels of crude oil have been transported by rail, increasing average transportation costs and putting increased pressure on the rail network running out of the region.

Despite government and industry efforts to increase capacity, it has not kept pace with supply growth, exerting downward pressure on crude oil benchmarks priced in Western Canada in 2018. This situation was exacerbated in the fall, when temporary refinery shutdowns in the U.S. Midwest disrupted the largest market for crude oil from Western Canada and sent several Canadian crude oil benchmarks to historically low levels.

Recently, Canadian benchmark prices have improved substantially after the refineries in the U.S. Midwest resumed normal operations and the Alberta government’s December announcement that it would begin to temporarily curtail oil production at the start of 2019. However, Canadian crude oil prices are expected to remain vulnerable to disruptions on a pressured export transportation network and to adverse supply or demand developments. This situation is expected to persist until one or more new major pipelines come on stream.

Budget 2019 Economic Outlook

The economic outlook has been revised moderately down since the 2018 Fall Economic Statement

The average of private sector forecasts has been used as the basis for fiscal planning since 1994 and introduces an element of independence into the Government’s economic and fiscal forecast. The Budget 2019 economic forecast presented in this section is based on a survey conducted in February 2019.

Reflecting expectations of slightly weaker economic growth in late 2018 and early 2019, the private sector economists have lowered their forecast for real GDP growth in 2019, to 1.8 per cent from 1.9 per cent anticipated in the 2018 Fall Economic Statement (Table A1.1). Over the five-year projection period, real GDP growth is expected to average 1.8 per cent—unchanged compared to the 2018 Fall Economic Statement.

The outlook for GDP inflation (the broadest measure of economy-wide inflation) has been revised down in 2019 to 1.6 per cent, compared to 2.0 per cent in the 2018 Fall Economic Statement, mainly reflecting terms of trade impacts of lower forecasted crude oil prices. As a result, the level of nominal GDP (the broadest measure of the tax base) is lower by an average of about $12 billion per year over the forecast horizon compared to the 2018 Fall Economic Statement.

|

|

2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

2018–

2023 |

|---|---|---|---|---|---|---|---|

| Real GDP growth1 | |||||||

| Budget 2018 | 2.1 | 1.6 | 1.7 | 1.6 | 1.8 | – | – |

| 2018 Fall Economic Statement | 1.9 | 1.9 | 1.6 | 1.6 | 1.9 | 1.9 | 1.8 |

| Budget 2019 | 1.9 | 1.8 | 1.6 | 1.7 | 1.9 | 1.9 | 1.8 |

| GDP inflation1 | |||||||

| Budget 2018 | 2.0 | 1.9 | 2.0 | 2.0 | 1.9 | – | – |

| 2018 Fall Economic Statement | 2.0 | 2.0 | 1.7 | 2.0 | 2.0 | 2.0 | 2.0 |

| Budget 2019 | 1.9 | 1.6 | 1.9 | 2.0 | 2.0 | 2.0 | 1.9 |

| Nominal GDP growth1 | |||||||

| Budget 2018 | 4.1 | 3.5 | 3.8 | 3.6 | 3.8 | – | – |

| 2018 Fall Economic Statement | 3.9 | 4.0 | 3.3 | 3.7 | 4.0 | 3.9 | 3.8 |

| Budget 2019 | 3.8 | 3.4 | 3.5 | 3.7 | 3.9 | 4.0 | 3.7 |

| Nominal GDP level1 (billions of dollars) | |||||||

| Budget 2018 | 2,229 | 2,307 | 2,395 | 2,482 | 2,576 | – | |

| 2018 Fall Economic Statement | 2,226 | 2,314 | 2,391 | 2,479 | 2,578 | 2,679 | |

| Budget 2019 | 2,223 | 2,298 | 2,379 | 2,467 | 2,564 | 2,667 | |

| Difference between Budget 2018 and Budget 2019 | -6 | -9 | -16 | -15 | -12 | – | – |

| Difference between 2018 Fall Economic Statement and Budget 2019 | -3 | -16 | -12 | -13 | -14 | -13 | -12 |

Budget 2019 Fiscal Outlook

The Government continues to manage deficits carefully while delivering real results that grow the economy, create jobs and improve the quality of life for the middle class and people working hard to join it.

In Budget 2019, the Government of Canada is introducing new investments to support workers, strengthen income security of seniors, bolster the health of Canadians and improve housing affordability, while maintaining the debt-to-GDP ratio on a downward track and protecting the long-term fiscal sustainability of Canada’s economy.

Table A1.2 outlines the fiscal impact of economic and fiscal developments since the 2018 Fall Economic Statement, including the cost of new measures announced in this budget.

Notably, 2018–19 monthly fiscal results have been better than expected since the 2018 Fall Economic Statement. The stronger-than-expected 2018–19 monthly fiscal results are primarily driven by higher income tax revenues, reflecting a strong labour market and higher corporate profits. The impact of the 2018–19 results partially carries forward over the forecast horizon, which more than offsets the impact of the downward revision to the economic growth outlook provided by private sector economists. Details of the Budget 2019 fiscal outlook are provided in Annex 2.

|

|

Projection | |||||

|---|---|---|---|---|---|---|

|

2018–

2019 |

2019–

2020 |

2020–

2021 |

2021–

2022 |

2022–

2023 |

2023–

2024 |

|

| FES 2018 budgetary balance1 | -18.1 | -19.6 | -18.1 | -15.1 | -12.6 | -11.4 |

| Adjustment for risk from FES 2018 | 3.0 | 3.0 | 3.0 | 3.0 | 3.0 | 3.0 |

| FES 2018 budgetary balance (without risk adjustment) |

-15.1 | -16.6 | -15.1 | -12.1 | -9.6 | -8.4 |

| Economic and fiscal developments since FES 2018 | 5.9 | 4.8 | 4.7 | 3.7 | 4.1 | 4.6 |

| Revised balance before policy actions and investments | -9.3 | -11.9 | -10.4 | -8.4 | -5.5 | -3.9 |

| Policy actions since FES 20182 | -1.4 | -1.0 | -0.6 | -0.6 | -0.2 | -0.2 |

| Investments in Budget 2019 | ||||||

| Investing in the Middle Class | 0.0 | -0.6 | -1.3 | -1.8 | -2.3 | -2.4 |

| Building a Better Canada | -3.2 | -0.3 | -0.8 | -0.8 | -0.6 | -0.4 |

| Advancing Reconciliation | -0.9 | -0.7 | -1.0 | -1.0 | -0.6 | -0.6 |

| Delivering Real Change | -0.1 | -1.7 | -1.6 | -0.8 | -0.5 | -0.6 |

| Other Budget 2019 investments3 | 0.0 | -0.7 | -0.9 | 1.6 | 0.6 | 1.2 |

| Total investments in Budget 2019 | -4.2 | -4.0 | -5.7 | -2.7 | -3.4 | -2.8 |

| Total policy actions and investments since FES 2018 | -5.6 | -5.0 | -6.3 | -3.3 | -3.6 | -2.9 |

| Budgetary balance | -14.9 | -16.8 | -16.7 | -11.8 | -9.1 | -6.8 |

| Adjustment for risk | -3.0 | -3.0 | -3.0 | -3.0 | -3.0 | |

| Final budgetary balance (with risk adjustment) |

-14.9 | -19.8 | -19.7 | -14.8 | -12.1 | -9.8 |

| Federal debt (per cent of GDP) | 30.8 | 30.7 | 30.5 | 30.0 | 29.3 | 28.6 |

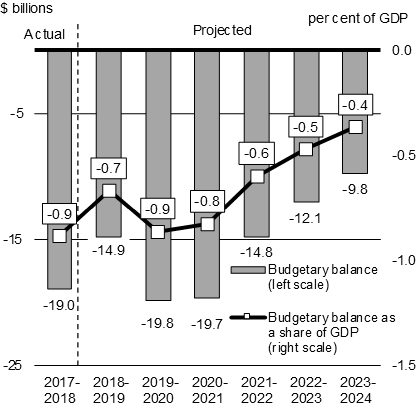

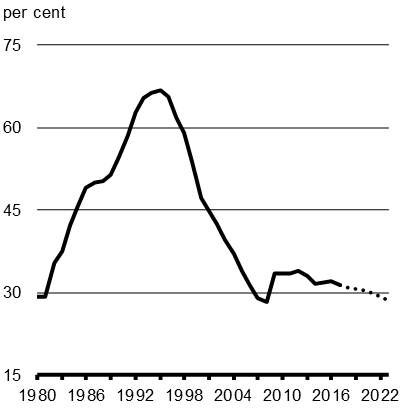

Budget 2019 continues to carefully manage deficits over the medium term. After including the measures proposed in this budget, the deficit is projected to decline from $19.8 billion in 2019–20 to $9.8 billion by 2023–24, with a projected continuous decline in the federal debt-to-GDP ratio, which is expected to reach 28.6 per cent in 2023–24 (Chart A1.11).

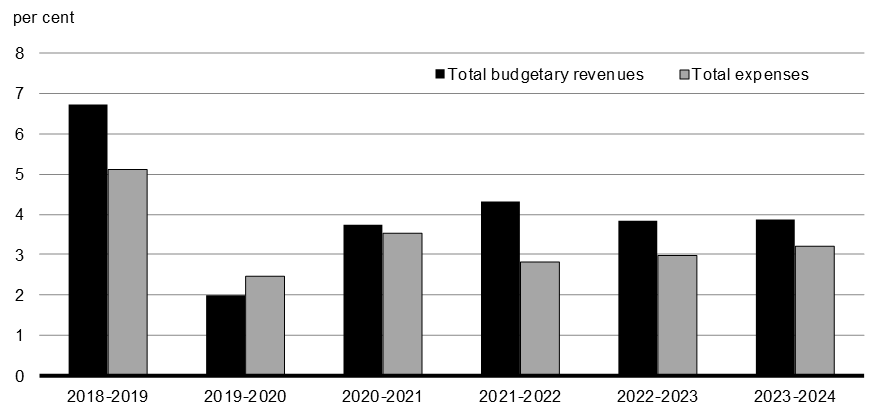

Budgetary revenues are expected to grow on average by 4.1 per cent annually over the forecast horizon, in line with economic growth over the period, while expenses are expected to grow at approximately 3.3 per cent per year (Chart 1.12). Notably, the decrease in revenue growth in 2019–20 is associated with the new tax incentives proposed in the 2018 Fall Economic Statement to encourage businesses to accelerate investment in capital, including the Accelerated Investment Incentive.

On average, budgetary revenues are expected to grow faster than expenses over the forecast horizon

Impact of Alternative Economic Scenarios

The fiscal projections presented in this budget are based on an average of the February 2019 private sector economic outlook survey. However, economists surveyed offered a wide range of views on future economic growth and the path of nominal GDP (the broadest measure of the tax base). Changes in economic growth assumptions can have large impacts on the budgetary balance and debt-to-GDP profile over an extended projection horizon.

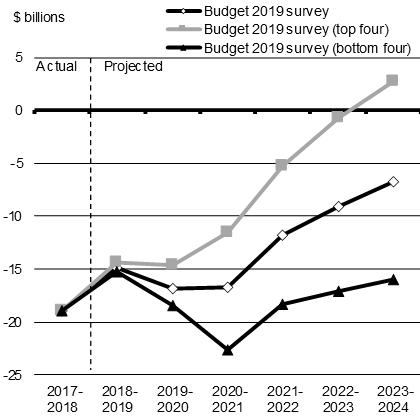

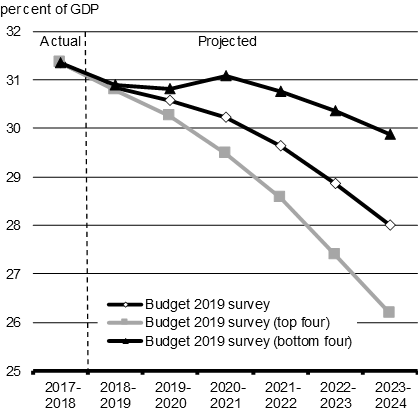

For example, if economic growth was stronger than expected, equaling the average of the top four individual forecasts for nominal GDP growth–which is equivalent to nominal GDP growth being 0.4 percentage points per year higher, on average, than the full February survey–the budgetary balance would improve by $5.4 billion per year (Chart A1.13).

Conversely, basing fiscal projections on the average of the bottom four individual forecasts for nominal GDP growth—which is equivalent to nominal GDP growth being 0.4 percentage points per year lower, on average, than in the full February survey—the budgetary balance would worsen by $5.3 billion per year on average, and the federal debt-to-GDP ratio would still decline, but would be 29.9 per cent in 2023–24.

- Date modified: